With the news today that inflation has risen over 5% and is at it’s highest point in 10 years. I’m doing some digging to understand how banks work, how it may affect interest rates, and what might this mean for house prices in 2022.

Part 1: Is an overview on how banks and lenders are affected by changes to the Bank of England Base rates.

——————————————————————————————————————-

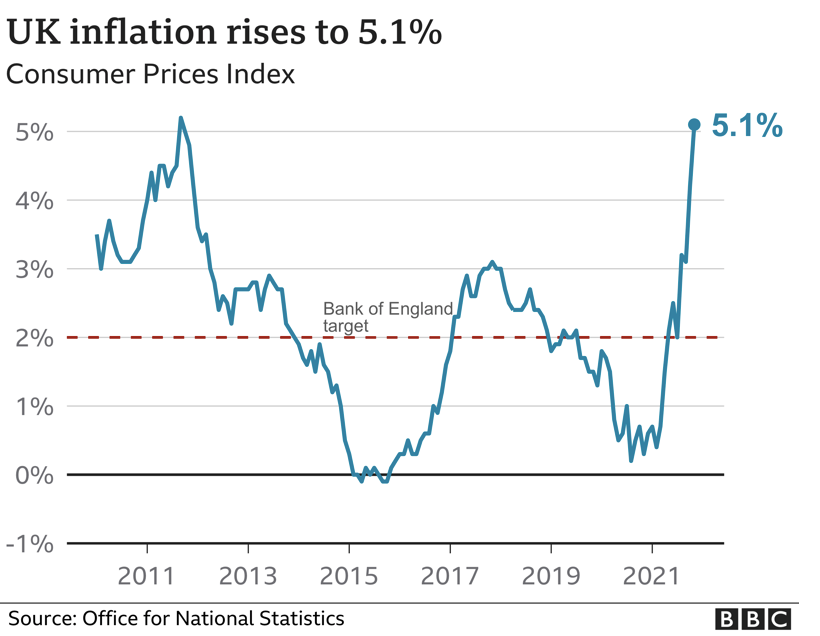

Inflation hits 10-year high as energy, fuel and clothing costs jump

The cost of living surged by 5.1% in the 12 months to November, up from 4.2% the month before, and its highest level since September 2011.

Higher transport and energy costs drove the rise, which was above forecasts of a 4.7% increase, the Office for National Statistics (ONS) said.

Its chief economist Grant Fitzner said more expensive fuel, energy, clothing and second hand cars were big factors.

The cost of raw materials also rose significantly, he added.

“A wide range of price rises contributed to another steep rise in inflation, which now stands at its highest rate for over a decade,” he said.

BBC headline, Dec 15th 2021

Does an increase in inflation automatically stimulate base rate rises?

When people think about inflation they often associate it with a Bank of England (BoE) interest rise to control the rise, is that likely to happen this time?

Well it’s not always the case that a change in the BoE’s rate, either up or down, flows directly through to the market. The reason for that is, because while residential mortgages and Buy to Let mortgages are mostly delivered by banks, they can also be delivered by lenders (as opposed to banks) in the form of bridging for commercial mortgages, development finance. These lenders may or may not be affected by the base rate, depending on where their finance comes from.

For banks, who deliver the majority of mortgages in the UK, the way the way an other business works, from a profit and loss point of view; If a mortgages is thought about as a loan, then a loan is a profit and loss statement. The first line of the spreadsheet is the income line, that reflects the interest and fees that you receive from delivering the loan product. Underneath that you’ve got all the costs that come with delivering the product (ie cost of operations; sales staff, underwriters, commissions etc). These are fixed costs and don’t change with the base rate.

In addition banks factor in a risk factor for bad debt, where they set aside a percentage of their income against possible default (unemployment escalation, covid increases, cost of living increase etc). And finally you have the cost of capital, which is where the base rate feeds into. All these factors mixed into together will produce an interest offer that they are comfortable with.

What you have seen, even though the BoE rates have been at record lows, there wasn’t much margin left on these loans and the cost of finance part of it was relatively small part of the mix. So there wasn’t much room for rates to come down. There wasn’t much room for banks to do a lot, even with base rate coming down because all of their other costs stayed the same.

With the challenger bank and lenders it depends on the sort of source of their funds. They may have had an injection from funds from hedge funds, pension funds, private individuals, so depending on what their particular situation is, they may or may not be directly affected by base rates changes.

Ultimately each bank or lender will have its own view on the world and that will drive the assumptions they make in modeling their loans and therefore where their pricing will go too.